2023 End of Year Market Update

December 30, 2023

December 30, 2023

2023 was a challenging year for the U.S. housing market: Mortgage rates reached a two-decade high, housing inventory stayed at historically low levels, and nationwide sales prices continued their upward trajectory, making homeownership a distant possibility for many. The concern over housing affordability persisted among homebuyers, justified by a substantial increase in mortgage payments since 2022, with a considerable number of homeowners allocating more than 30% of their income to monthly payments. Consequently, sales of existing homes faced a sluggish year, while the scarcity of existing-home inventory contributed to a steady rise in sales of new residential homes compared to the previous year.

Higher mortgage rates have repercussions beyond potential homebuyers. Numerous existing homeowners acquired or refinanced their properties in 2020 or 2021, securing mortgages with rates significantly lower than those prevailing today. While these pandemic-era mortgages have proven advantageous for many, they have also become a deterrent for some to relocate. Instead of relinquishing their favorable mortgage rates for higher ones and incurring a more costly monthly payment, certain prospective sellers have opted to delay their plans to move. This decision has added to the scarcity of homes for sale, contributing to an increase in home prices.

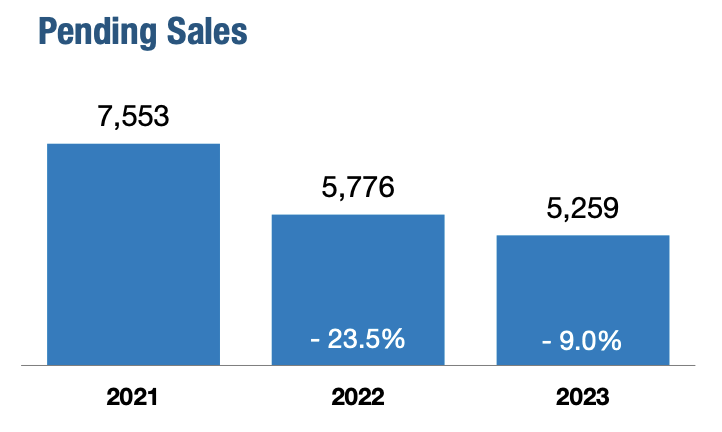

Pending sales decreased 9.0 percent, finishing 2023 at 5,259. Closed sales were down 7.5 percent to end the year at 5,405.

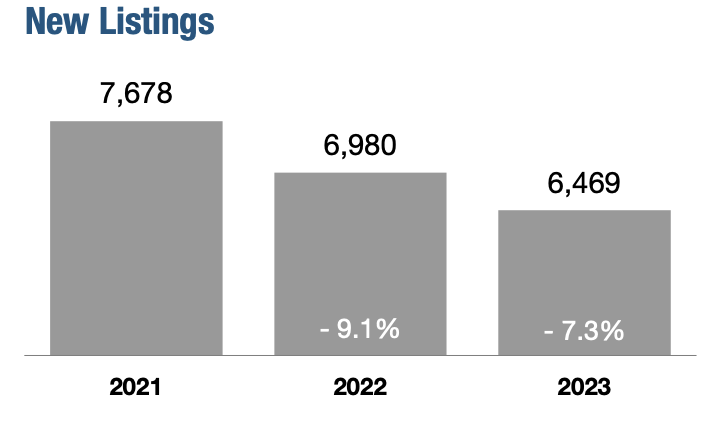

Comparing 2023 to the prior year, the number of homes available for sale was up by 23.3 percent. There were 1,299 active listings at the end of 2023. New listings decreased by 7.3 percent to finish the year at 6,469.

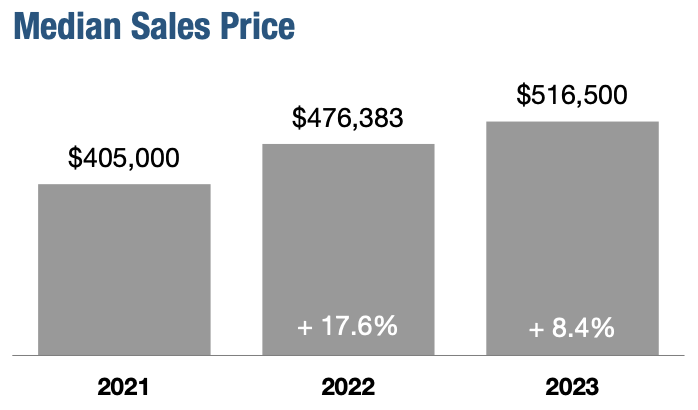

Home prices were up compared to last year. The overall median sales price increased 8.4 percent to $516,500 for the year. Detached home prices were up 4.5 percent compared to last year, and attached home prices were up 15.3 percent.

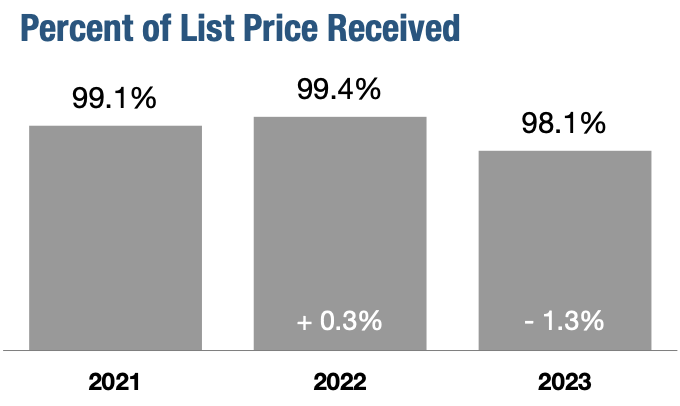

Sellers received, on average, 98.1 percent of their original list price at sale, a year-over-year decrease of 1.3 percent.

With indications of improvement in inflation, the Federal Reserve has recently declared a halt to further increases in interest rates, planning at least three cuts to their benchmark rate in 2024. The decline in mortgage rates over recent months is expected to reinvigorate interest from both buyers and sellers, potentially resulting in an upswing in both home sales and housing supply. Nonetheless, challenges in affordability are anticipated for many homebuyers, and economists forecast that U.S. home sales will likely remain below levels observed from 2019 to 2022. Regarding home prices, opinions diverge, as some analysts foresee stability or continued growth in certain areas, while others anticipate a modest price decline in specific markets.

Information and Infographics courtesy of RESIDES, INC. Current as of January 10, 2024.

Inventory is steadily growing, with active listings up nearly 29% and months of supply increasing to 4.8.

Fall in the Lowcountry brings a refreshing change from the warm summer days.

Recent headlines may leave you wondering what’s next for mortgage rates.

If you’re taking a look at your expenses as you retire, saving money where you can has a lot of appeal.

If you're thinking of selling your house this spring, now is the perfect time to start getting it ready.

Overarching story is that prices went up last year, not down. Let’s dive into the data to set the record straight.

The answer is complicated because there’s a lot that can influence mortgage rates.

You’re juggling a mix of excitement about what’s ahead and feeling little sentimental about your current home.

Higher mortgage rates have repercussions beyond potential homebuyers.

Whether you’re buying your first home, selling a luxury property, or investing in Hilton Head Island real estate, Tyler Stone provides expert guidance, local knowledge, and a client-focused approach. From the initial consultation to closing, he ensures a smooth, stress-free experience tailored to your unique goals.